27 February 2026

Welcome to the Sixteenth Edition of The Inside Track!

Every month brings new headlines, new certainty, and new reasons to act. Most of them will not matter five years from now.

Greenland has attracted renewed international attention for a place best known for ice. Award ceremonies have doubled as cultural battlegrounds. In some corners of the world, constitutional norms have begun to look more like flexible guidelines. And gold has reminded South Africa that sometimes a metal can do more for a budget than a committee.

Tickets for next year’s Rugby World Cup in Australia sold out within minutes. The second release opens in May. I was fortunate enough to secure quarter-final seats, with the hope of a Springbok clash with New Zealand. Planning ahead, it seems, is still fashionable in at least one arena.

Markets, meanwhile, have been quietly processing all of it.

Since the beginning of the year, a great deal has shifted beneath the surface. In this edition, I’ll bring you up to speed on the budget, the global backdrop, and a few market themes that are beginning to matter more than the noise.

Let’s get into it.

Market Indicators

Returns % to 20 February 2026

| 1 Month | YTD | 1 Year | |

|---|---|---|---|

| SA Equity (ALSI) | 2.1 | 6.29 | 43.08 |

| SA Bonds (ALBI) | 4.3 | 3.4 | 28.6 |

| SA Property (ALPI) | 5.5 | 6.9 | 44.02 |

| SA Cash (Avg. SA Money Market Fund) | 0.54 | 0.55 | 7.31 |

| Global Markets (MSCI ACWI in ZAR) | 0.88 | 0.59 | 5.55 |

| Global Markets (MSCI ACWI in USD) | 3.8 | 3.89 | 20.84 |

| USD/ZAR - R15.98/USD at 23 February 2026, negative number indicates appreciation of the rand | -1.43 | -3.26 | -12.73 |

Market Pulse

Local markets continue to lead. Over the past 12 months, South African equities, listed property, and bonds have delivered strong returns. Year-to-date performance remains positive. Cash is steady but modest. Offshore returns in rands look softer, largely due to a stronger rand rather than weak global markets.

Inflation, interest rates, and Federal Reserve policy remain part of the macro backdrop. The more visible risk in the US indices is concentration. A large share of performance is being driven by a small group of technology companies. This year, several are meaningfully increasing leverage to fund the AI race. They will not all be winners. Whether this spending translates into durable productivity and earnings growth remains uncertain. As expectations, concentration, and leverage rise together, the margin for disappointment narrows.

Back home, basic materials have driven much of the recent momentum. How long that lasts is unclear. If you do not own gold shares directly, there is little reason for concern. Gold already carries meaningful weight in the JSE indices, so diversified portfolios typically have exposure.

Overall, the backdrop remains supportive. Concentration and leverage in global markets are worth monitoring, particularly when recent performance begins to feel easy.

What’s Worth Noticing

On the Local Front

South Africa’s 2026 Budget sets the framework for tax, spending, and incentives at home. These are the key changes that matter most for household cash flow, investors, and long-term planning.

1. TFSA (Tax-Free Savings Account)

- Annual contribution limit increased from R36,000 to R46,000 (from 1 March 2026)

- Lifetime TFSA limit remains at R500,000

- National Treasury confirmed the lifetime limit was not increased in this budget

2. Retirement Fund Contribution Deduction

- Annual deduction limit increased from R350,000 to R430,000, subject to the existing cap of 27.5% of taxable income (effective from 1 March 2026).

3. Capital Gains Tax (CGT) Thresholds

- Annual exclusion of capital gains or losses increased from R40,000 to R50,000

-

Exclusion on death increased from R300,000 to R440,000

-

Primary residence CGT exclusion increased from R2,000,000 to R3,000,000

4. Small Business Thresholds

-

Turnover tax threshold for micro businesses increased from R1,000,000 to R2,300,000

-

Compulsory VAT registration limit increased from R1,000,000 to R2,300,000 (effective 1 April 2026)

5. Retirement Interest and Living Annuity Thresholds

-

Retirement interest de minimis threshold increased from R247,500 to R360,000

-

Living annuity commutation threshold increased from R125,000 to R150,000 (applies 1 March 2026)

6. Estate and Donations Tax

-

Donations tax exemption increased from R100,000 to R150,000 per donor per year

-

Estate duty increases to 25% for estates above R30 million

7. Personal Income Tax Adjustments

-

Personal income tax brackets and medical tax credits will be fully adjusted for inflation for the first time in three years

-

Other related tax thresholds and limits are also adjusted for inflation

8. No Major Tax Increases

-

A previously pencilled R20 billion tax increase was removed

-

Corporate tax rates remain unchanged

-

VAT rate remains unchanged

-

Sugar tax remains unchanged

9. Levies and Taxes on Consumption

-

Fuel levy increases by 9c/l for petrol and 8c/l for diesel

-

Road Accident Fund (RAF) levy increases by 7c/l to R2.25/l (from 1 April)

-

Carbon tax increases from R236 to R308 per tonne CO₂ equivalent (from 1 Jan 2026)

-

Carbon fuel levy increases to 19c/l for petrol and 23c/l for diesel (from 1 April)

-

Diamond export levy increases by 5%

10. Public Sector and Economic Assumptions

-

Public sector wages: average increase of approximately 4.4%

-

GDP growth forecast for 2026: 1.6%

-

Inflation forecast: 3.4%

-

Household consumption growth forecast: 1.8%

On the Global Stage

-

The recent State of the Union, which ran for nearly two hours, added colour, though less clarity on policy direction.

-

US inflation cooled to 2.4%, its lowest level since mid-2025, reinforcing expectations of potential Fed rate cuts later this year

-

Bond yields eased, with the 10-year Treasury drifting toward 4% as markets priced a more accommodative policy path

-

The US dollar softened modestly, supporting global risk assets and easing financial conditions.

-

European growth remained subdued, strengthening the case for ECB easing despite a continued trade surplus.

-

Geopolitical tensions remain elevated, with developments in the Middle East and renewed US–Iran negotiations keeping energy markets sensitive.

First Principles

A deep understanding of something does not automatically make it a compelling investment. You can understand a company, a technology, or crypto extremely well and still end up with a poor investment outcome.

Knowing the story is not the same as having a margin of safety, a sensible valuation, or a reliable return profile. Crypto is a useful case study. The technology may be sophisticated. The communities are engaged. The narratives are powerful. But price still matters. Liquidity still matters. Behaviour still matters. Markets require willing buyers at the price you need to sell.

Six months ago, conviction was high. Today, Ethereum has been down roughly 54% and Bitcoin close to 40% at various points. Volatility of that magnitude may be tolerable when an asset is purely speculative or earmarked for legacy purposes. It becomes far more complex when that same asset is expected to fund income. Stability and liquidity start to matter.

The lesson isn’t to predict better. It is to diversify thoughtfully, remain alert to confirmation bias, and be clear about the role each asset class plays within a long-term plan.

How Good Intentions Sometimes Unravel

When Tax Efficiency Becomes the Immediate Investment Strategy

Tax matters. But when tax becomes the dominant driver of decisions, other risks often get pushed into the background.

Liquidity, flexibility, concentration, and timing all still matter. A structure that is efficient on paper but fragile in real life can be expensive in ways that never show up in a tax calculation.

Food for Thought

The Difference Between Being Rich and Being Free

Being rich is about how much you have.

Being free is about how little you need from the world to live the life you want.

Two people can have the same net worth and completely different levels of freedom, depending on their fixed costs, obligations, and lifestyle assumptions.

Real financial progress often comes less from adding more, and more from needing less.

That does not mean living small. It means living deliberately.

Freedom is a balance sheet problem and a lifestyle design problem at the same time.

Quietly Interesting

-

22.4%: Bakkies make up 22.4% of all motorised vehicles in South Africa. The only class of vehicle that saw a reduction in its population last year was the minibus.

-

10%: South Africa occupies about 1% of the world’s land area, yet is home to almost 10% of the world’s known bird, fish and plant species. A quietly impressive slice of global biodiversity.

-

Early risers: South Africans reportedly have one of the earliest average wake-up times in the world.

-

Longest route: Route 62, running through South Africa, is one of the longest wine routes in the world at over 500 miles.

-

World first: South Africa was the first country in the world to include environmental rights in its constitution, giving everyone the right to an environment that is not harmful to their health or wellbeing.

Quote for the Month

“What matters is not whether an idea is true, but whether it works.”

— George Soros

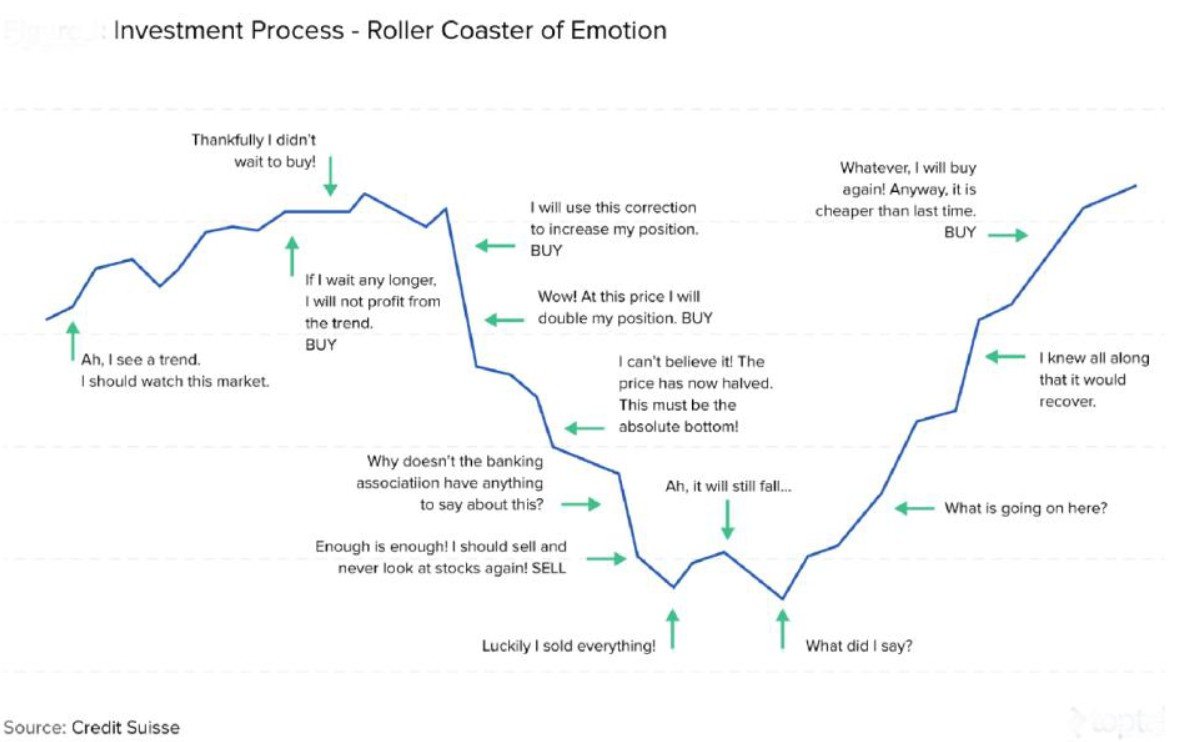

Visual For the Month

This chart shows the emotional roller coaster most investors ride in every market cycle. Prices move, but bad decisions are driven by fear, greed, and hindsight at exactly the wrong moments.

The real enemy isn’t volatility, it’s behaviour. And if you believe you are immune to emotion or ingrained bias, you may be uniquely qualified to assist Elon with Optimus.

Perspective for the Long Run

The Three-Layer Plan (And Why Most People Only Build One)

Most people think they have a financial plan. In reality, they usually only have a portfolio.

That is layer one.

Layer two is cash flow. Where does money come from when markets are down? Which assets get used first? Which ones are protected? How many years of spending are insulated from market noise?

Layer three is behaviour. What will you actually do when markets fall 20 or 30 percent? What is allowed to change? What is explicitly not allowed to change?

Here is the uncomfortable truth. A portfolio without a cash flow plan is fragile. A cash flow plan without behavioural rules is theoretical.

The real work of planning is not picking funds. It is designing a system that still works when the environment is hostile and your emotions are loud.

We are wired to prefer predictability. We check the weather. We read forecasts. Our brains prefer certainty because uncertainty is cognitively expensive. It creates mental strain and demands ongoing evaluation. The problem is that the events that really test a plan are almost never the ones we feel comfortable predicting.

The financial impact of Covid and the global financial crisis was a useful reminder. Many people felt they were financially fine and assumed life would simply carry on, until they discovered how fragile their setup really was. Too much debt. Too little flexibility. Not enough runway. The stress did not come from markets alone. It came from not having a system built to cope with disruption.

That is the real point of planning. Not to guess the next crisis, but to make sure your life still works when one inevitably shows up.

I hope this month’s mailer offered something useful to think about. The next one will be out toward the end of March 2026.

Until then, I’m always just a click away.

Take care, and enjoy the moments that matter.

Rob

Reference: Morningstar, Forbes, NinetyOne, Blackrock, Bloomberg, Capital Group, Reuters, Credit Suisse

Copyright (C) 2026 Stocks+Wealth Financial Planning. All rights reserved.

You are receiving this email because you are an existing client or agreed to receive information from Robert Taylor.

Our mailing address is:

Stocks+Wealth Financial Planning, 16 Virginia Ave, Vredehoek, Cape Town,Western Cape, 8001, South Africa

The information contained in this message is intended only for the recipient and may be a confidential client communication or may otherwise be privileged and confidential and protected from disclosure. If the reader of this message is not the intended recipient, or an employee or agent responsible for delivering this message to the intended recipient, please be aware that any dissemination or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately notify us by replying to the message and deleting it from your computer.

Please also be aware that the contents of this email include the opinions of the sender Robert Taylor and are not to be construed as advice or acted or before consulting with Robert Taylor or any other licensed Financial Services Provider where professional process and the FAIS act and General Code of Conduct are applied.