29 April 2026

Welcome to the Seventeenth Edition of The Inside Track.

Just as it seemed things were settling, it is a reminder of how easily conditions can change.

Basing future decisions on past trajectory, in other words recency bias, can lead to the assumption that what has worked will continue. In practice, that is rarely what makes for sound investing. At its core, investing is a risk management process, and that is particularly evident in periods like this.

The past two months have been a reminder of how quickly markets can shift when events move beyond economics.

The escalation in the Middle East has unsettled global markets. What began as a relatively stable outlook, with easing inflation and expected rate cuts, has changed quite abruptly.

South Africa entered this period from a stronger position than in previous years. Inflation was contained, interest rates had started to ease, and there were early signs of improvement. This has helped soften the initial impact, although the rand has weakened and volatility has returned.

This has not been a gradual shift in the cycle, but a significant change in conditions.

The questions now are what is driving this volatility, how it is being transmitted through markets, and what it means for portfolios and new capital.

Market Indicators

Returns % (to 24 April 2026)

| 1 Month | YTD | 1 Year | |

|---|---|---|---|

| SA Equity (ALSI) | 6.3 | 2.2 | 33.2 |

| SA Bonds (ALBI) | 3.2 | 0.8 | 23.8 |

| SA Property (ALPI) | 5.3 | 1.0 | 31.4 |

| SA Cash (Avg. SA Money Market Fund) | 0.6 | 2.1 | 7.2 |

| Global Markets (MSCI ACWI in ZAR) | 5.7 | 6.1 | 17.2 |

| Global Markets (MSCI ACWI in USD) | 9.0 | 6.1 | 32.6 |

| USD/ZAR - R16.53/USD at 28 April 2026, negative number indicates appreciation of the rand | -3 | 0.0 | -11.6 |

Market Pulse: A Quick Read on the Numbers Above

Over the past two months, equity markets have been under pressure, particularly in emerging markets, following the escalation in the Middle East. The JSE reflects how quickly changes in outlook can affect sectors, especially those linked to commodities. For investors, decisions based on past trajectory or market enthusiasm can be misleading.

Gold has given back some of its recent gains, with a stronger US dollar and weaker rand weighing on the price in the short term.

Bonds have also come under pressure as expectations of interest rates adjust. Given the inverse relationship, this has led to weaker bond performance and has also filtered through to listed property.

As noted previously, interest rates remain a key driver across asset classes, often acting as a trigger for broader repricing.

While the adjustment has been uncomfortable, it has also led to a reset in certain areas of the market.

One positive development is that technology sector valuations have become more aligned with value compared to the start of the year.

More broadly, periods of volatility tend to reintroduce a degree of realism into pricing. Assets that had moved ahead of underlying fundamentals begin to reflect a wider range of outcomes, which can improve the long-term starting point for investors.

This does not remove uncertainty, but it does begin to restore balance between risk and return.

PS: Good investing is not about making the right call all the time, it’s about structuring things so you can survive when you’re wrong

Key Global Market Insights

By now, the Strait of Hormuz has become a familiar name. A few months ago, it sat quietly in the background. Today, it is a reminder of how quickly distant events can become relevant when they begin to affect everyday costs.

It is a narrow stretch of water through which close to 20% of the world’s oil flows each day, a reminder that small places can have outsized consequences.

As energy costs rise, this feeds into inflation, which in turn influences interest rate expectations. Interest rates sit at the centre of how markets are priced.

When they move higher, the value of future earnings and income is reduced, placing pressure on both equities and bonds.

What begins as a geopolitical event can move through the system quickly, affecting valuations across markets.

Key South African Market Insights

-

Bitcoin: Proposed changes from National Treasury would bring digital assets into South Africa’s exchange control framework. The draft introduces reporting requirements and oversight of how these assets are held and transferred. Some industry responses suggest this could include limits on personal holdings and conversion above certain thresholds into rand.

-

Treasury says South Africa has enough fiscal space to extend the fuel-tax cut by two months, providing up to R12 billion in relief to cushion consumers from the oil shock linked to the Iran War.

-

The IMF has lowered South Africa’s 2026 growth forecast to around 1%, down from 1.4% earlier this year, reflecting pressure from higher oil prices and disruptions to fuel imports.

Blind Spots That Can Undermine Wealth and Peace of Mind

A common pattern is to prioritise lifestyle commitments ahead of building investments, often with the assumption that current income will continue.

Homes and day-to-day costs expand first, with investing left to what remains. Over time, this delays asset growth and limits compounding.

Many individuals also remain heavily weighted towards South African assets, exposing their wealth to slower growth and currency weakness relative to developed markets.

This matters, as many of the goods and services we rely on, including technology and specialised healthcare, are priced in US dollars, pounds, and euros.

Wealth is built by reversing that order, investing first and spending second, and allocating to assets that can grow across different economies and currencies.

Food for Thought

A documentary worth noting, Everyone Is Lying to You for Money, takes a closer look at the crypto industry.

It focuses less on the technology itself, and more on how the space has been promoted, the incentives behind it, and some of the high-profile failures along the way, including the collapse of FTX.

It does not attempt to label the entire space, but instead raises questions around speculation, behaviour, and how investment narratives take hold, particularly during periods of strong returns.

Whether one agrees with its conclusions or not, it offers a different perspective on how markets evolve and how investor behaviour is shaped.

In my experience, markets reveal intent through behaviour. When something is consistently held rather than used, it begins to function less like a currency and more like an asset.

Time will tell how those two paradigms coexist in the same space.

Quote for the Month

“The essence of investment management is the management of risks, not the management of returns.”

Benjamin Graham

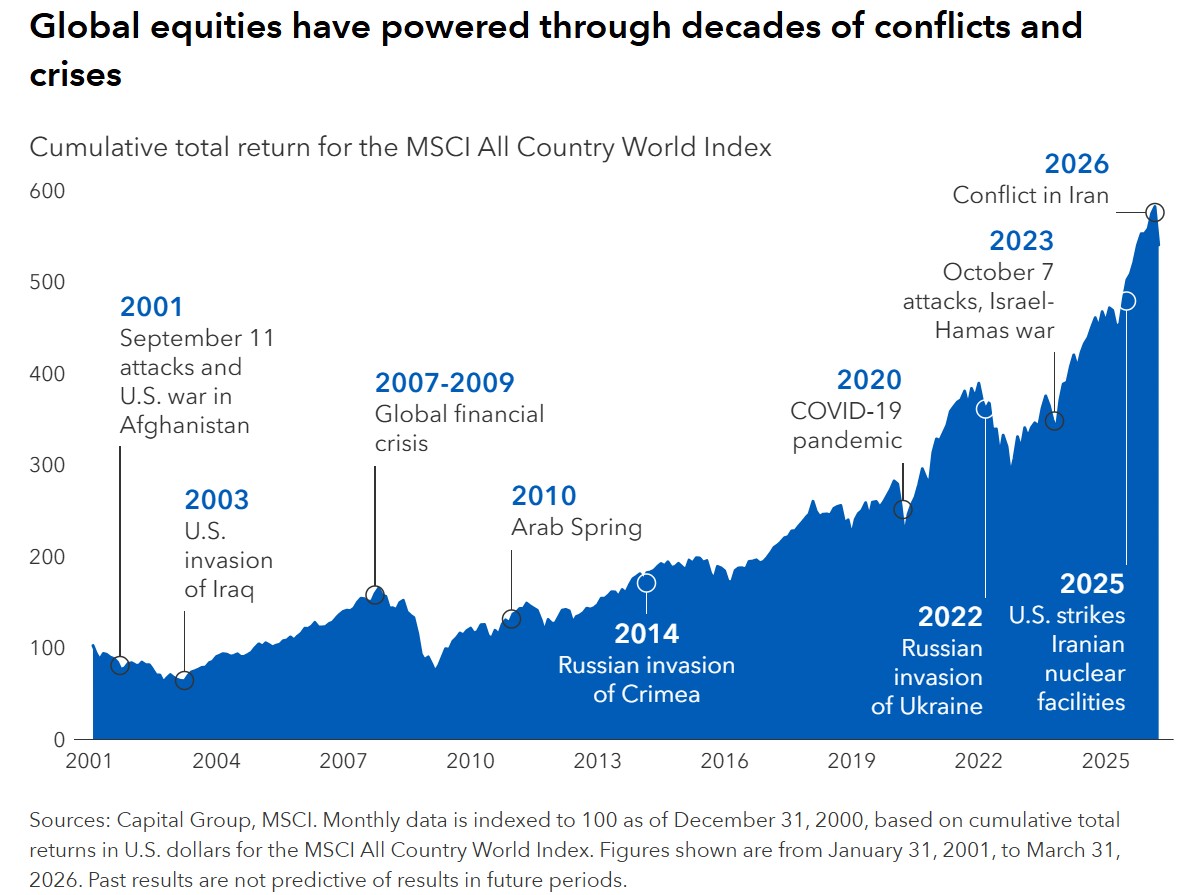

Visual For the Month

The visual above shows that volatility is not separate from good outcomes, but part of the process that leads to long-term growth.

Many of the investments that go on to deliver strong long-term outcomes do not do so in a straight line. Periods of volatility, uncertainty, and being out of favour are part of the journey.

It can feel uncomfortable while it is happening, but it is not unusual. In many cases, it is during these periods that opportunities begin to form.

Perspective for the Long Run

Information vs integration

There is no shortage of information available today. Tools, platforms, and even AI can provide quick answers to specific financial questions.

That can be useful, at least on the surface.

The challenge is that financial decisions don’t exist in isolation. Tax, risk, liquidity, time horizon, and objectives are all connected.

A decision that makes sense on its own can have unintended consequences elsewhere. Even portfolios that appear diversified can carry significant overlap beneath the surface. When a macro event occurs, a large portion of the portfolio can move in the same direction, often leaving investors questioning why.

Good answers to individual questions don’t always add up to a good overall plan.

The question is simple: if everything moved at once, would your portfolio behave the way you expect it to?

I hope this month’s mailer gave you something valuable to think about. Looking forward to catching up again at the end of May.

Until then, and as always, I’m just a click away.

Take care, stay mindful, and enjoy the moments that matter.

Reference: Morningstar, Forbes, NinetyOne, Blackrock, Bloomberg, Capital Group, Reuters

Copyright (C) 2026 Stocks+Wealth Financial Planning. All rights reserved.

You are receiving this email because you are an existing client or agreed to receive information from Robert Taylor.

Our mailing address is:

Stocks+Wealth Financial Planning, 16 Virginia Ave, Vredehoek, Cape Town,Western Cape, 8001, South Africa

The information contained in this message is intended only for the recipient and may be a confidential client communication or may otherwise be privileged and confidential and protected from disclosure. If the reader of this message is not the intended recipient, or an employee or agent responsible for delivering this message to the intended recipient, please be aware that any dissemination or copying of this communication is strictly prohibited. If you have received this communication in error, please immediately notify us by replying to the message and deleting it from your computer.

Please also be aware that the contents of this email include the opinions of the sender Robert Taylor and are not to be construed as advice or acted or before consulting with Robert Taylor or any other licensed Financial Services Provider where professional process and the FAIS act and General Code of Conduct are applied.